by Rory Fabian

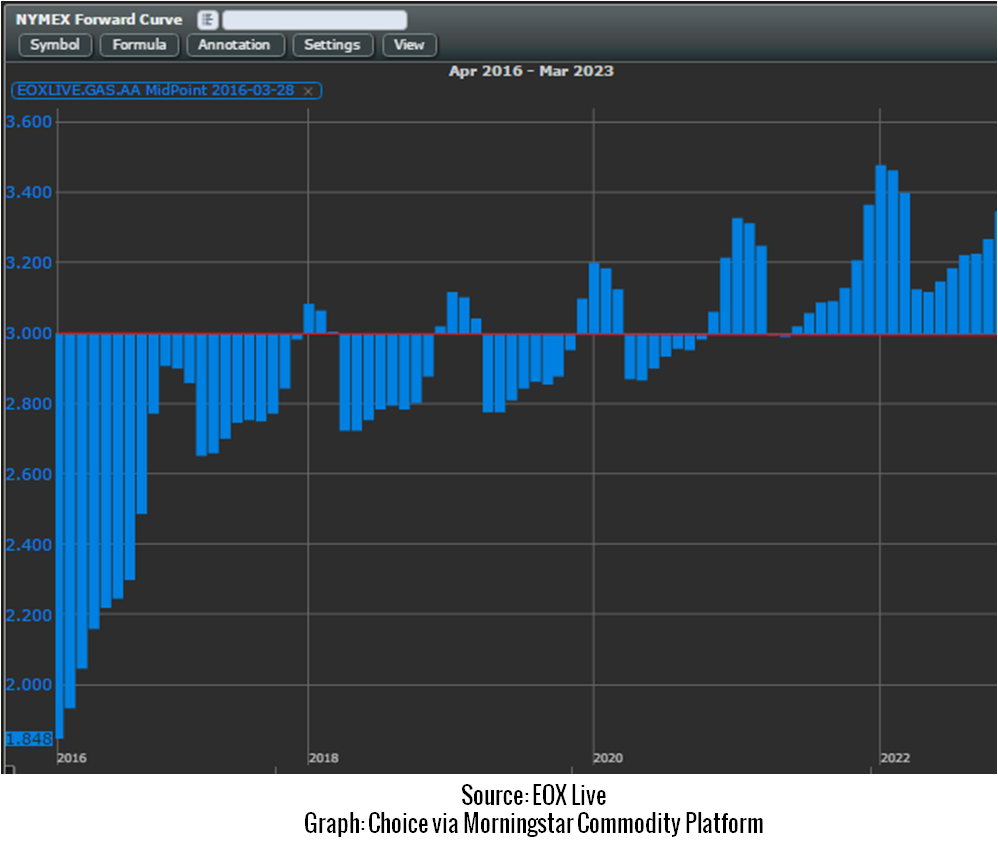

Before the recent uptick in pricing of natural gas, we were seeing NYMEX at its lowest levels in YEARS. This was tremendous news for the end user because, as we know, electricity pricing will go down if Natural Gas is cheap, right? Well, natural gas, among other commodities, plays a big role in the price of electricity to the end user because much of the generation uses commodities as a fuel to generate electricity. However, actual energy has become (although still a large part) a smaller slice of the proverbial supply pie (see What’s This in My Supply Contract?). Some may look at their electricity bill in recent years and see that their price per kWh may be stagnant or even higher despite the recent low in commodity pricing.

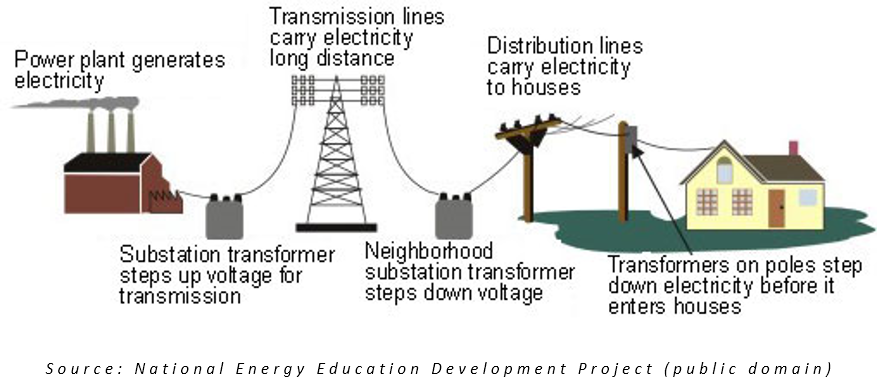

A major factor in electricity pricing has been the transmission and distribution portion of the bill. Transmission has to do with the handling of bulk transfer of power from generation facilities to local substations. From there distribution takes over in the form of local wiring between the substations and end user.

Transmission & Distribution

We hear over and over about our Nation’s infrastructure and how it is deteriorating. Our roads, bridges, tunnels, etc are in need up a major face lift. Well our electrical grid is in need of the same treatment. In PJM, there are plans in place for a major overhaul in Transmission systems to upgrade for reliability, efficiency, or performance standards. Not all of the cost, but some of the money that is dumped into these projects are passed along to the end user, of course – you may see this on your electricity bill, contract or letter from your supplier as NITS (Network Integration Transmission Service). Don’t expect these charges to decrease anytime soon, as many load zones have plans in place for additional upgrades in power lines beyond 2018.

Distribution is no different. Local utilities must ensure that their customers will have reliable systems for improved performance and stability. Overall, this will benefit the end user – I remember when Hurricane Sandy hit, I was without power for weeks. Hopefully, with the upgrades at the local level, the utilities will be able to ultimately cut costs and increase local reliability for the grid.

So, What Now?

Transmission and Distribution upgrades are a necessary function of the electricity grid just like upgrades to highways, bridges, and tunnels. So what can you do in the meantime to reduce transmission and distribution costs? Well, for commercial and industrial customers can reduce their bill through demand response or capacity management projects to reduce peak load. Managing of peak load will reduce strain on the grid and result in more $$ in your pocket.

Natural gas and overall commodity pricing is still one of the big, big driving factors in electricity pricing. However, due to structural improvements in the grid, we are seeing a stagnation or increase in $/kWh on our monthly bill. Unless end-users take a look at energy management solutions or adjusting their internal systems, they shouldn’t be surprised if the electricity bill keeps going up, up and away.

Confidential: Choice Energy Services Retail, LP.