by Rory Fabian

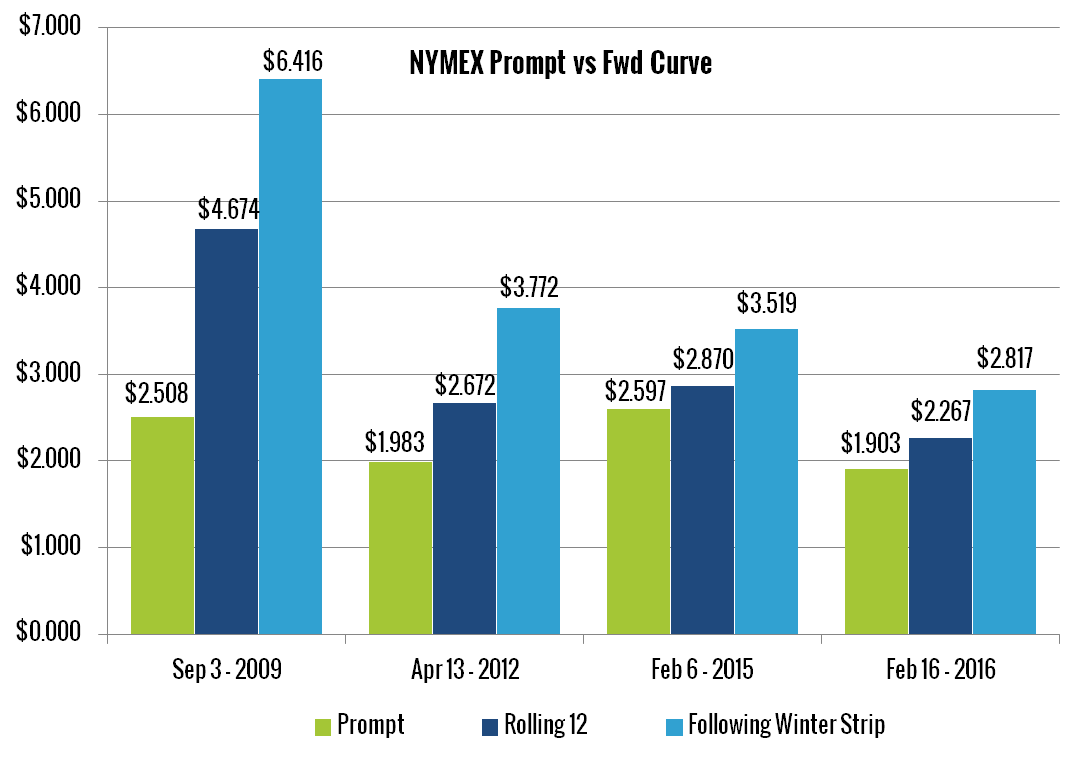

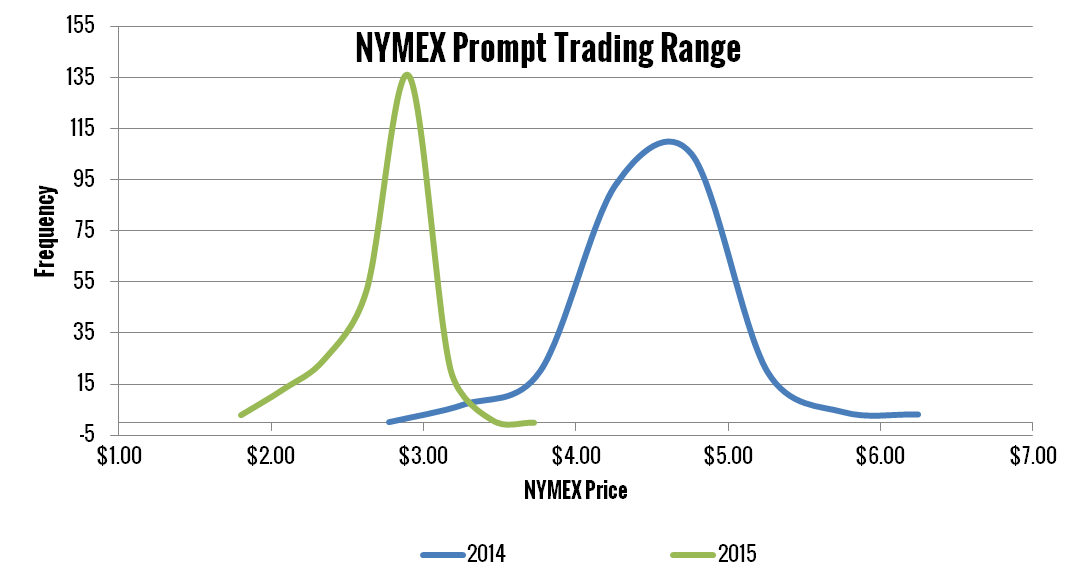

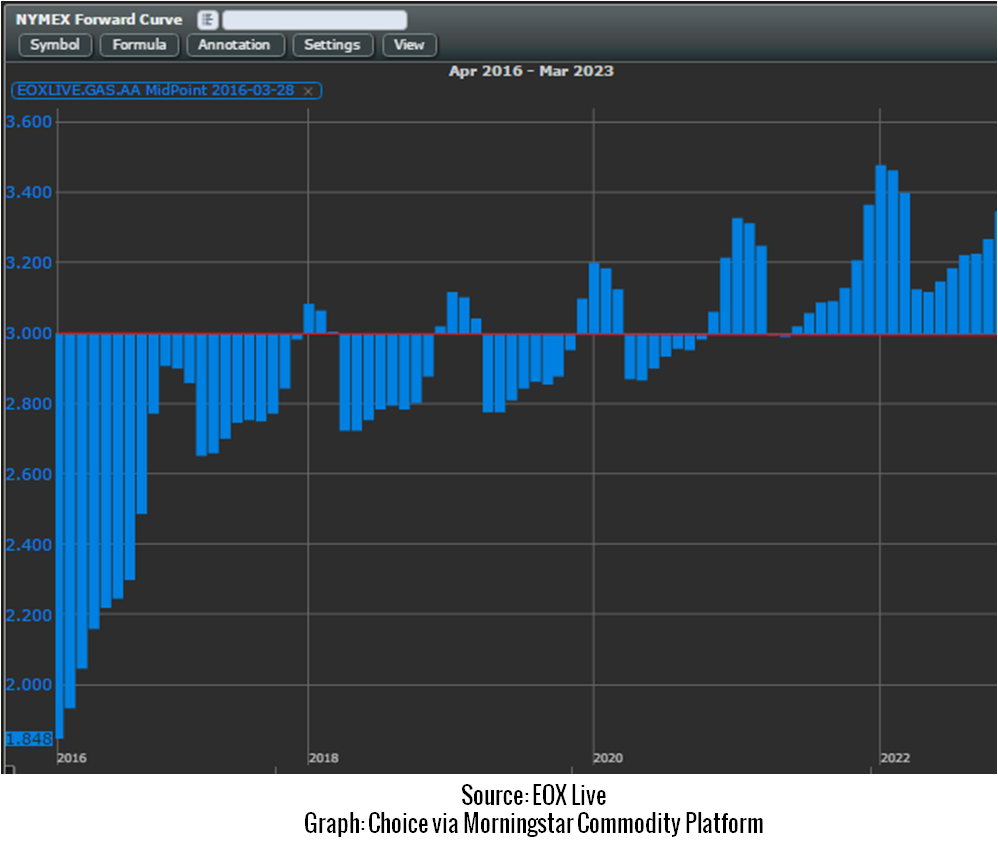

As if 2015 energy prices were not low enough, Q1 of 2016 has been defined by historic low energy pricing. Prompt month natural gas pricing has been trading below the $2.00/MMBtu mark since early February. The forward curve isn’t much better, as the NYMEX natural gas curve does not trade above $3.00/MMBtu till 2018! As Choice has discussed in other blog entries and white papers, the low pricing can be contributed to many factors such as: record production, STRONG storage levels, and bearish weather over the last couple of months. However, even with the low prices, for both prompt month gas and for the extended curve, reaction has been mixed by end-users. Many are excited about the opportunity and are locking up pricing for the long-term. Others are less than enthusiastic and are in no rush to secure their energy commodity price. Today, we will take a closer look at the two camps of clients – opposing mindsets – the “Git-R- Done” group and the “Hurry Up and Wait” crowd.

“Git-R-Done”

Prompt natural gas pricing is below $2.00/MMBtu and the rest of the curve is flatter than Rickie Fowler’s hat! To put in perspective, the forward curve hasn’t been this low since you thought dial up internet was the greatest thing in the world (You Got Mail). As a result, many end-users are locking their commodity prices now and locking it long-term. While there is a chance that pricing may go even lower, end-users in the “Git-R-Done” bucket are taking the risk off the table now instead of waiting to try find the bottom of the market.

The “Git-R-Done” group also realizes that pricing at these levels will not last forever. It didn’t take long for the market to rebound in 2012 when prompt month gas dropped below $2.00/MMBtu, and it could happen quickly again. Bullish movers such as natural gas exports (LNG and Mexico), declining rig counts, and a potential for a hot summer all have the ability to bring the supply/demand picture back in balance for natural gas. With end-users now seeing drastic savings over their previous energy contract, the “Git-R-Done” crowd wants to strike now.

“Hurry Up and Wait”

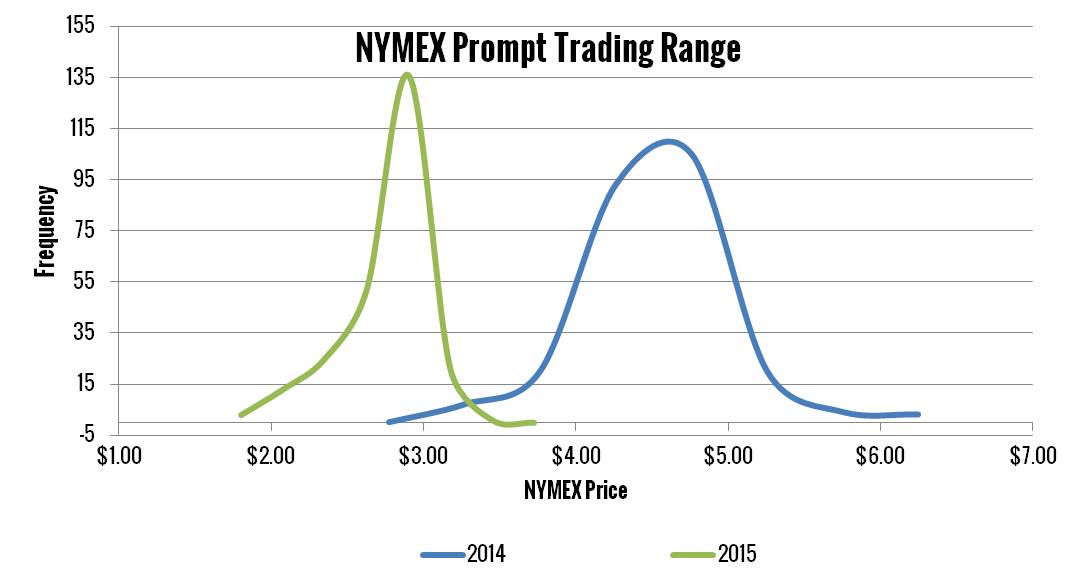

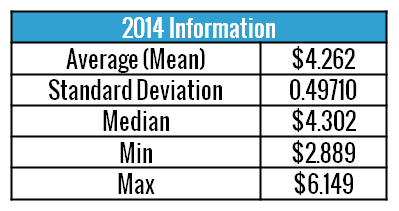

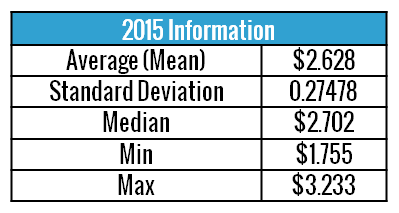

The second camp is the “Hurry Up and Wait” sector. They are well aware that natural gas has been trading below $2.00/MMBtu since early February, but lower energy prices are becoming old news. They were told the prices in 2015 were low, when the market was consistently below $3.00/MMBtu and traded range bound the entire year. Pricing in 2016 has only dropped further from the “low” 2015 price levels so why should end-users lock now.

Additionally, there is no shortage of bearish news in the market. Storage levels are at record levels with the potential to break storage capacity levels at the end of injection season. Weather has been bearish all year with warmer than normal temperatures in the North, and mild temperatures in Texas. And even though the natural gas market is dealing with depleting rig counts and decreased associated gas from oil, production levels have remained at historic high levels. Record production has been buoyed by an increased drilling efficiency, especially in the Marcellus Shale gas play. With so much bearish news-what’s the hurry?

Conclusion

What is the correct move here – “Hurry Up and Wait” or “Git-R-Done”? It depends on the goal of the end-user. If the goal is to get the lowest price possible, then we will have to wait till the end of the year to see which group was correct in 2016. However, with many end-users (especially many of our clients) wanting budget certainty while obtaining contract over contract savings, the “Git-R-Done” crowd is gaining strong momentum.

Confidential: Choice Energy Services Retail, LP.